You are either going to find this post fascinating and very usable or the most boring post I have ever done, next to this one. However, I have been doing a lot of research lately at work on women, money and the economy so I feel like this is something worth sharing and I hope you find it useful ~ knowledge is key. I am not offering advice {I am by no means an expert on mortgages} just some thoughts to get you thinking ~ and since most of my readers are women I hope you find this message empowering.

I went online to make a payment on our mortgage the other day and our lender has a built-in amortization schedule and calculators {very cool}. I got to playing with it and it has consumed my thoughts since that point and I am hoping if even one person learns something from this post, my job is done! 🙂

Amortization schedules/tables fascinate me. Seriously. If you don’t know what one is {hopefully you all do} it is essentially a schedule that shows how much of your monthly mortgage payment goes to principal and how much goes to interest for all the months of your loan. When I was in graduate school they made us calculate these out by hand for practice and I thought they were fun. Weird, I know. I love calculating extra payments here and there to find out how much you can ultimately save. It can actually be pretty fun. Until you start playing with real money.

There is something so intriguing/infuriating to me about this process. Most people know an insane amount of your mortgage payment goes to interest each month {especially early on in your loan}. But, when you stare at the cold, hard numbers {the amortization schedule}, it makes you mad. Most people end up paying MORE THAN DOUBLE the amount they took out for the loan due to the amount of interest they are paying off. Again this is fairly common knowledge. But, what those mortgage companies don’t tell you is how little, additional payments here and there can make a huge impact in paying your mortgage off sooner {and ultimately paying a fraction of the interest}.

If you haven’t played with amortization calculators online, don’t be intimated. Just Google ‘Amortization Calculator’ to get tons of results – this one from BankRate.com works well {but there are others that will calculate savings too}. Usually they require the loan amount and terms {length and interest rate} and you can find out how making an additional payment to principal each month {regardless of amount} can shave years off of your mortgage. Remember, those extra payments don’t just remove that amount from the loan – it is that amount plus interest on that amount for the remaining months/years on your mortgage that you end up saving.

For example. Take a $200,000 30-year mortgage at 6% interest. By simply paying $15 extra per month, you shave a year off the length of the mortgage {so you only pay that flat mortgage rate for 29 years rather than 30 years}. If you up that to $50 extra per month, your shave off three years. $100 takes off more than six years!

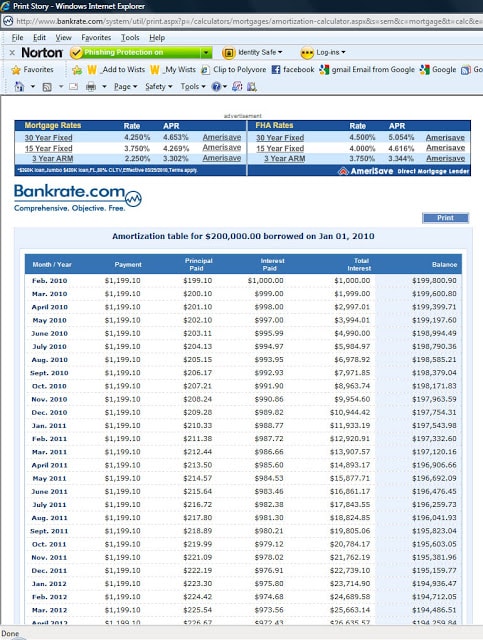

See the screen shot below for the first few years amortization table without any additional payments. In this example, the mortgage payment is $1,199.10 every month. However, you can see the amount applied to principal and the amount applied to interest of that $1,199.10 each month changes. In the first month, only $199.10 is applied to the principal, so even though you have paid nearly $1,200 your loan balance is only reduced by $199. The rest went to interest! Anything additional you pay each month gets knocked of the principal (the loan balance) at 100% since your interest payment was already made in the mortgage payment. The results can have huge impacts. In this example, if you were to see the end of the amortization schedule, this person has paid $231,676.38 in interest on a $200,000 loan. So, essentially you have paid $431,676.38 on the life of this loan.

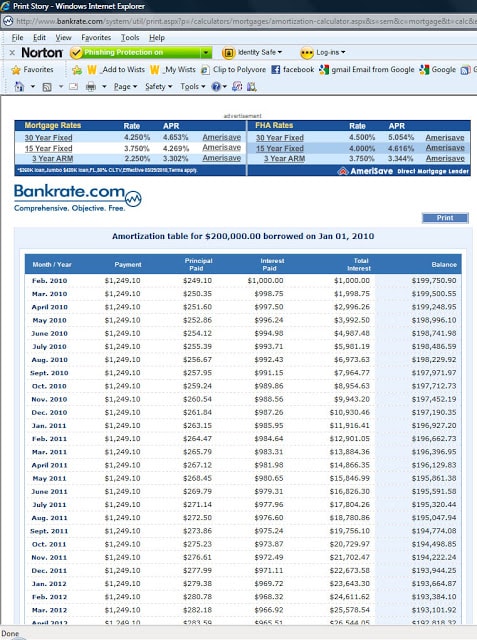

Here is the same case but with the additional $50 made each month to the prinicipal. Even in the first 24+ months, the results are dramatic so imagine what this can do on a 30-year mortgage! In this example, the person has paid $203,797.07 in interest on a $200,000 loan for a total of $403,797.07 paid. Still a lot of money, but a savings of $27,879.31 over not paying anything additional per month.

Remember ~ you are not locked into paying the extra amount every month. So if you have a spare $75 this month but times are tough next month, you aren’t tied in to the additional payment when you are manually making the extra payment. Something else worth noting is that you may need to specify on your payment that it is to be applied to principal rather than as a deduction of next months payment {we have to do this with our mortgage company}. Additionally, by making extra payments to principal, you still must pay the pre-determined mortgage payment each month {meaning you can’t skip a month a year from now because you were paying extra}. Again, I am not an expert in the mortgage arena so it is wise to check with your lender for any other stipulations to making additional principal payments.

I know economically times are tough right now, but if you have any extra money you can commit to setting aside each month to apply to an additional payment to your principal each month, it can make a huge impact in the long run. It is important to check with your lender to ensure there are not any fees involved with an early payoff, etc. {not that common any longer}. It is also important to not put all your extra money into your mortgage, as it is also important to have about three-six months of income in a savings account if possible to help cover any unexpected expenses or emergencies. Check with your financial planner if you need advice on how much extra you should pay.

I have decided to think twice about the purchases I make and decide if it is worth instant gratification now or if it is better to apply that extra money to our mortgage. Granted, many times the instant gratification wins out for me, but, there are many other times that I end up not buying something because of this little thought in the back of my head. By saving a little extra now to apply to your mortgage payment will mean huge returns in the future!

Hopefully you find this interesting and it makes you as mad as it makes me. And by mad, I mean taking action to combat all that interest and committing to find ways to paying your mortgage off sooner. Obviously you know where I stand since I devoted 30 minutes to ranting on and on about this. Thanks for those that made it to the end while I was on my little soapbox! 🙂

If you would like to follow along on more of my home decor, DIY, lifestyle, travel and other posts, I’d love to have you follow me on any of the following:

Pinterest / Instagram / Facebook / Twitter / Bloglovin’ / Google

Leave a Reply